The Tax Cuts and Jobs Act of 2018 is the most extensive tax change legislation to be passed in the past 30 years. It effectively cuts individual, corporate and estate tax rates with the intention of fostering economic growth. With the title of “An Act to Provide for Reconciliation Pursuant to Titles II and V of the Concurrent Resolution on the Budget for Fiscal Year 2018”, it is not surprising that our tax professionals have been consuming many cups of coffee as they work to understand and apply the changes made in the legislation to 2017 taxes and for tax planning for upcoming seasons.

In our February newsletter, we focused on the changes in the legislation that affect homeowners. Although there is some overlap, this month we will explore the bill’s additional impact on individual taxpayers. As noted previously, many of these personal deductions will expire in December of 2025. Business changes are meant to be permanent.

The changes involve so many parts of the tax code that how the tax bill will affect you depends on your personal situation — how many children you have, how much you pay in mortgage interest and state/local taxes, your salary and where in the country you live, among many variables. We will attempt to clarify as many of these categories as possible, but it will be very important to contact us for a tax projection to learn how these changes might affect your individual situation.

In this issue, we will look at:

- Income Tax Rates and Brackets

- The Standard Deduction and Itemized Deductions

- The Child Tax Credit

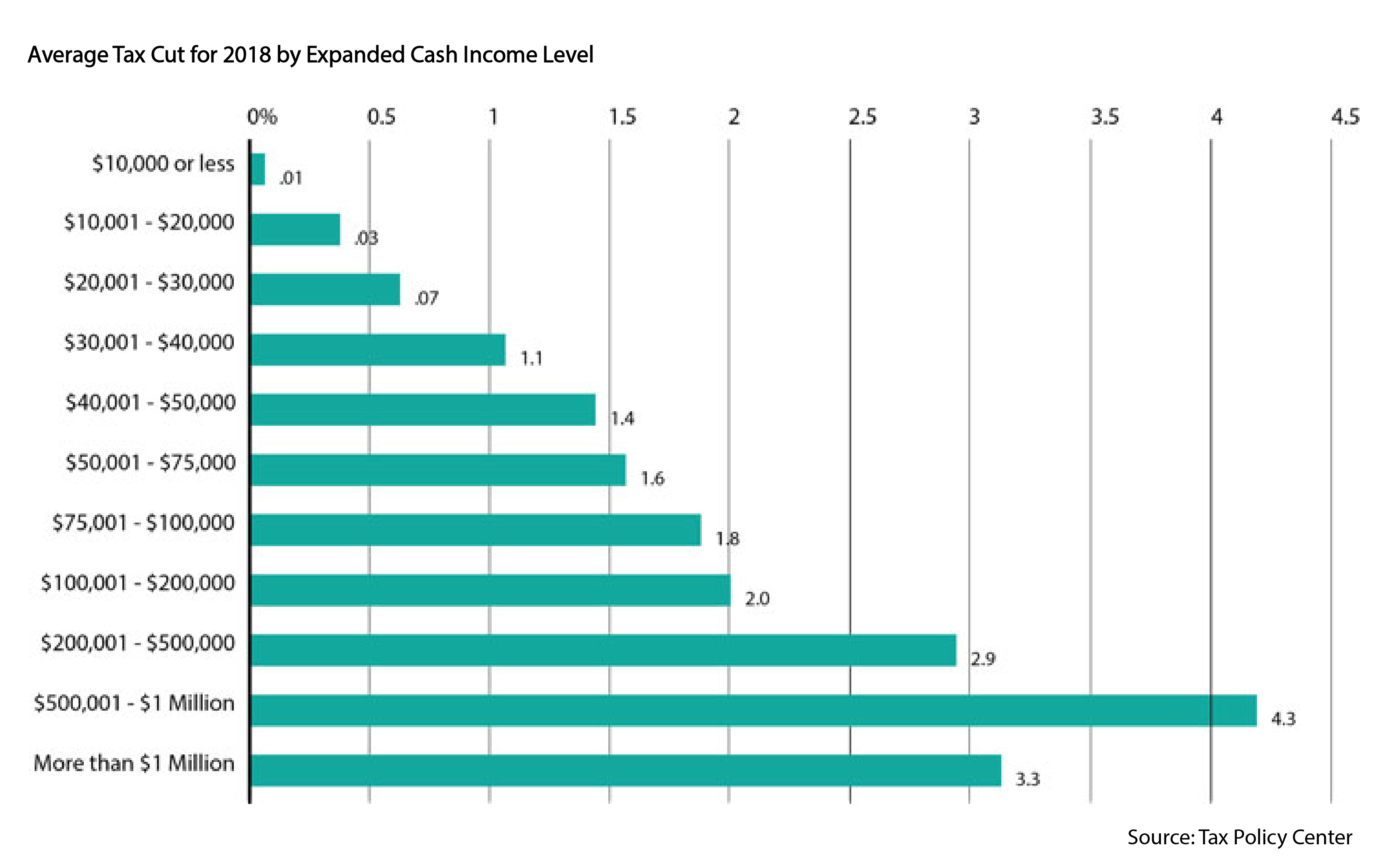

How will Your Income Tax Bracket Change?

These changes for individuals will expire in 2025 absent further legislation. According to the Tax Policy Center, every taxpayer, on average, will save something from the tax bracket changes. Those in the highest income households will see the most savings.

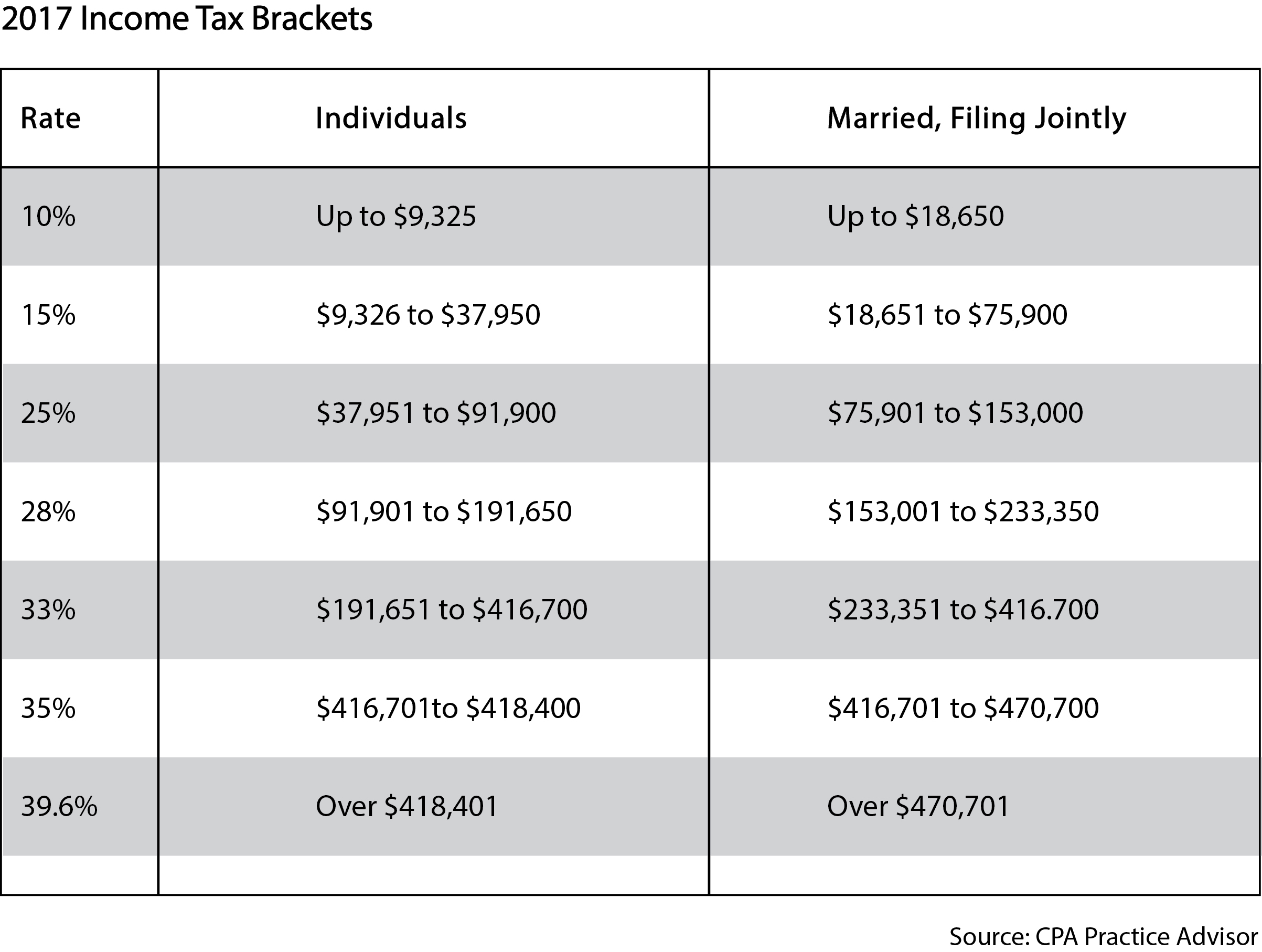

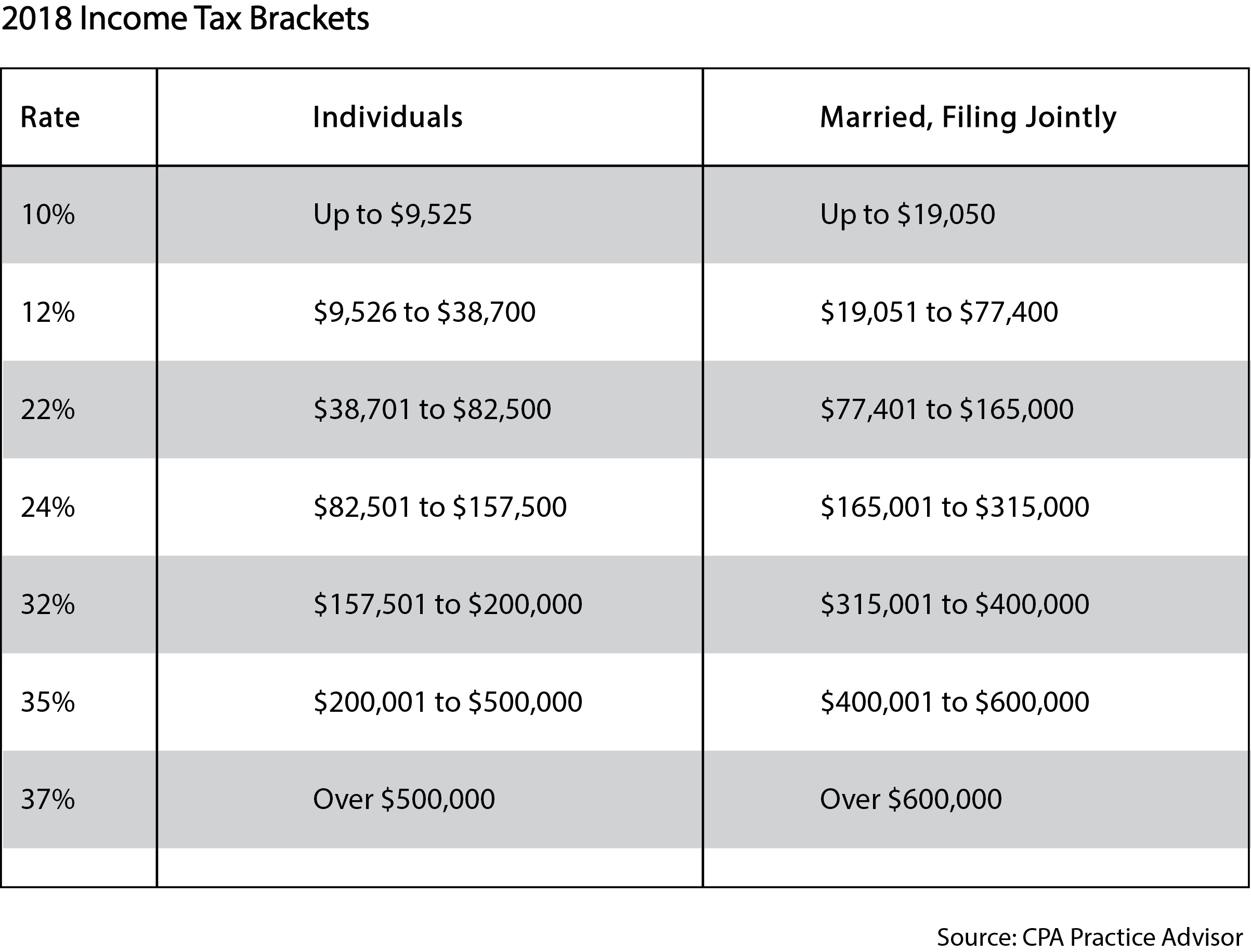

The 2018 Tax Act retains the same number of tax brackets as the previous year but decreases the percentage rate for all categories with the exception of the 10% bracket. The distribution of the income levels within each group has also changed significantly, especially in the upper brackets.

Tax Brackets and Inflation

The tax brackets will now be indexed to a slower inflation measure called the Chained Consumer Price Index for All Urban Consumers.i Previously, the brackets were indexed by the Consumer Price Index (CPI). Chained CPA is a variant under which tax breaks would grow more slowly.

According to Bloomberg.com: “Both are reported monthly by the U.S. Labor Department’s Bureau of Labor Statistics, and both track the prices of a "basket" of 80,000 goods and services bought by consumers in urban areas. But chained CPI adjusts for what’s known as substitution bias by recognizing that consumers tend to shift their purchasing behavior as the relative prices of things change. For example, when the price of Granny Smith apples increases, people may buy Gala apples instead. ii

As a result, chained CPI shows a slower pace of price gains, or inflation, than traditional CPI, and as a result a more gradual increase in the upper limits for each tax bracket. If wages start to increase at a faster rate than the chained CPI, taxpayers could find part of their income being taxed at the rates on the next bracket.

The change to Chained CPI will also have an impact on social programs such as Social Security that are tied into inflation which may mean benefits growing at a slower pace than they have under CPI. iii

The Standard Deduction and Exemptions

For many years now, the tax law has allowed taxpayers to claim “exemptions” for each individual or dependent that is part of their household. In 2018, that exemption/deduction will be eliminated. Instead, the standard deduction will effectively be doubled potentially offsetting the loss of the exemptions. Whether the larger standard deduction and lower tax rates will result in decreased tax liabilities will depend on your personal circumstances.

iv

Under the new legislation, the larger standard deduction and elimination of itemized deductions as noted in our last article may result in households electing not to itemize their deductions on Schedule A as they had done in previous years. The Joint Committee on Taxation estimates that 94% of taxpayers will claim the standard deduction as opposed to the 70% who currently claim it now. v These changes were intended to simplify tax preparation and record keeping.

As a refresher, here is a list of itemized deductions that have changed or will no longer be deductible:

- Casualty and Theft Losses.

These are no longer tax deductible unless the government has formally declared your area to be a federal disaster area will you be able to claim losses from hurricanes, fires, floods and snow or ice events.

- Medical Expenses.

While medical expenses can still be deducted if you are itemizing, the rate shifts. For 2017 and 2018, they are deductible if they exceed 7.5% of adjusted gross income, down from the current 10%, allowing for more expenses to actually be deductible. This applies through 2019 and then returns to the 10% threshold.

- State and local taxes.

Taxpayers can deduct a maximum of $10,000 from the total of their state and local income taxes or sales taxes, and their property taxes (added together), a measure that might hurt itemizers in high-tax states such as California, New York and New Jersey. The $10,000 cap applies whether you are single or married filing jointly; if you are married filing separately, it drops to $5,000.

- Eliminated Miscellaneous Deductions.

Taxpayers lose the ability to deduct the cost of tax preparation, investment fees, bike commuting ($20/month), unreimbursed job expenses and moving expenses.

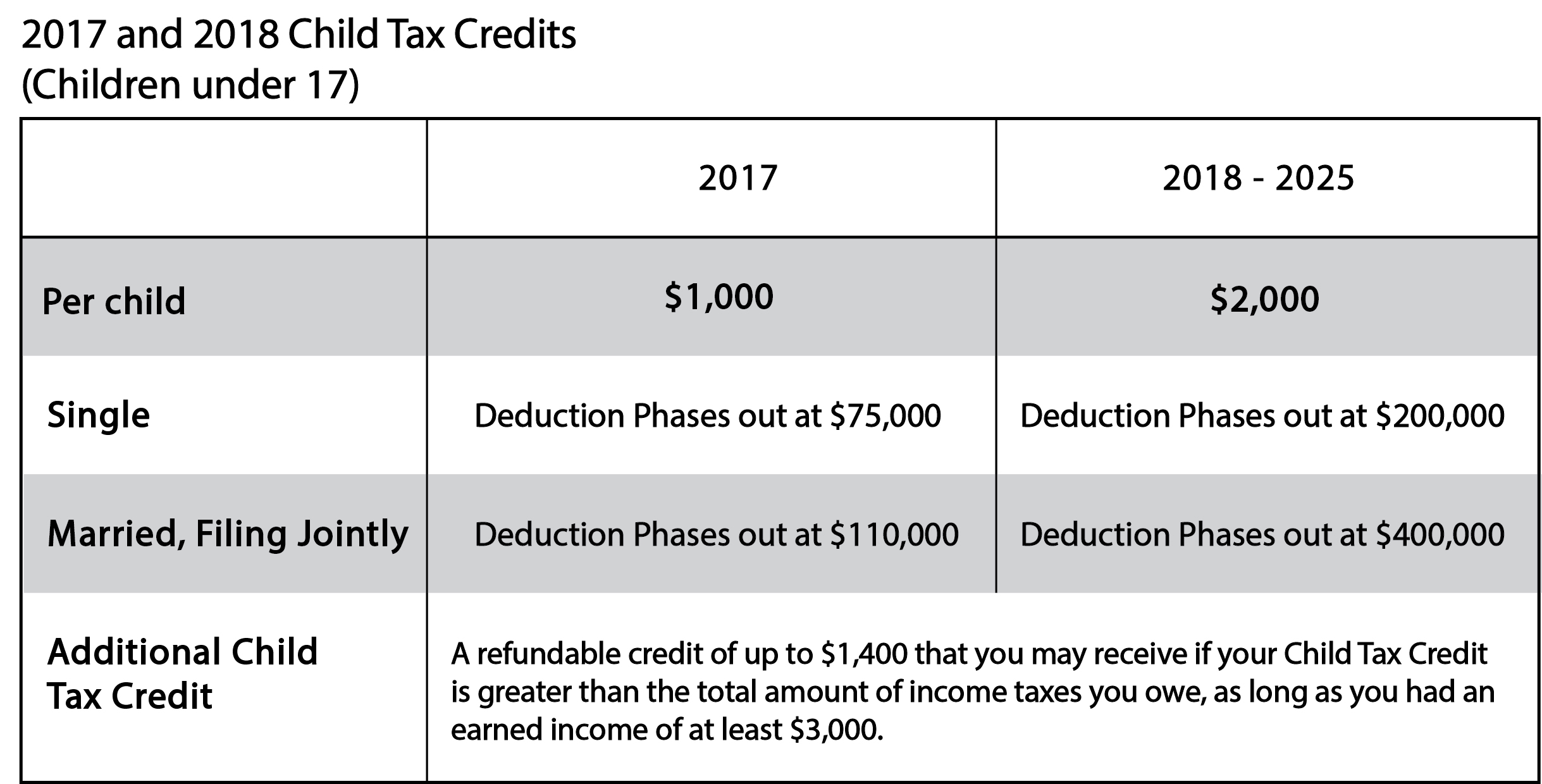

The Child & Dependent Tax Credits

The 2018 Tax Cuts and Jobs Act doubles the Child Tax Credit from $1,000 to $2,000 and expands the income thresholds that allow application of the credit.

For other dependents who are not “qualifying children” (as defined in the pre-2018 tax law), taxpayers are now able to claim a new non-refundable $500 credit that is subject to same income limits as the Child Tax Credits.

The tax bill does retain the Child and Dependent Care Credit, which is different than the Child Tax Credit. This credit which allows a taxpayer to seek or generate earned income is available for care related expenses for a qualifying child under the age of 13, a disabled spouse, or other qualifying persons.

Given the complexity of these changes, we strongly encourage you to consult with Shapiro Financial Security’s CPA’s so you can maximize your return for 2017 and plan effectively for future years. Please call us at 732-739-8991.